Machine Learning and High Dimensional Economics

My interest in information diffusion and computational economics led me to examine better ways to deal with high-dimensionality in macroeconomics taking inspiration from computer science, statistics, and computational sciences literature.

The broad goals of this research agenda are to:

- attack the curse of dimensionality in macroeconomics by combining economic models with new machine learning techniques.

- tie together models of statical learning from the agent’s perspective given non-trivial heterogeneity (i.e., using “learning” models from computer science/statistics literature inside of the agent’s problem, where the state may have high degrees of heterogeneity). The main applications are models of learning and inference in finance.

- chase especially useful spillovers that may come along the way (e.g., high-dimensional fixed-effects and sojourns into Bayesian methods).

For macroeconomics, this hybrid approach is especially important: we need to use the flexible non-parametric features of neural networks/deep learning with constraints and models that come out of economics. As an analogy, consider “Physics Informed Neural Networks” and scientific machine learning.

For more background, watch this excellent keynote from Karen Willcox

.I am on the Advisory Committee of the NumFOCUS supported SciML organization created to unify the packages for scientific machine learning.

Research

Solving Models of Economic Dynamics with Ridgeless Kernel Regressions

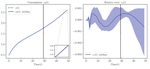

Spooky Boundaries at a Distance: Inductive Bias and Dynamic Macroeconomic Models

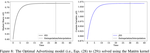

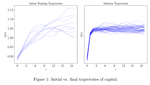

Taming the Curse of Dimensionality: Quantitative Economics with Deep Learning

Differentiable State-Space Models and Hamiltonian Monte Carlo Estimation